According to Gallup’s annual Economy and Personal Finance survey, conducted in April of 2013, over 60% of Americans do not have a written or computerized budget for their personal finances. SIXTY PERCENT!!! At first I was astounded, that is, until I reflected upon my own finances. After looking back on the years when we accumulated excess consumer debt, I realized it was directly correlated with NOT PLANNING (or maybe even not USING THE PLAN). Although, by nature, I am a planner, there were months, particularly after having kids, when we just needed diapers, milk, or even medicine, and the diapers, milk and medicine just kept accumulating on our credit cards. Due to exhaustion, sleep deprivation and the newness of being a parent, going over a budget was just not at the top of my list. As a result, we paid for the poor financial choices we made. Thankfully, we have since acknowledged our damaging decisions and over the last few years have gotten back on track. But it was not without significant loss to our personal finances.

[featured-image]

I have now come to understand, at the end of the day, if you do not take control of your finances (no matter how sleep deprived you are), it will take control of you.

We have learned:

“(To) tell our money where to go instead of wondering where it went.” John Maxwell

“(That) when there is no vision, the people perish” Proverbs 29:18

“And…a foolish man spends it all.” Proverbs 22:7

I do not want to be labeled a fool, nor do I want my money to perish while trying to figure out where it went. So, in order not to continue repeating the same mistakes, we created a plan—our monthly budget. As mentioned in previous blogs, we plan the year before. We determine what we will pay off and create our monthly budget accordingly.

So how do you create a budget?

- Calculate your total net income (how much you actually receive after taxes) including your spouse’s, if married.

- Calculate your monthly expenses

- If your total net income is LESS than your monthly expenses, you need to begin the “process of elimination”. Lower your cable plan, cell phone plan, eating out expenses, and whatever else you can think of. Eliminate and reduce expenses as much as you can until your monthly expenses are LESS than your net income.

- Once you have extra money remaining (after the elimination process), assign that to a bill you will pay off.

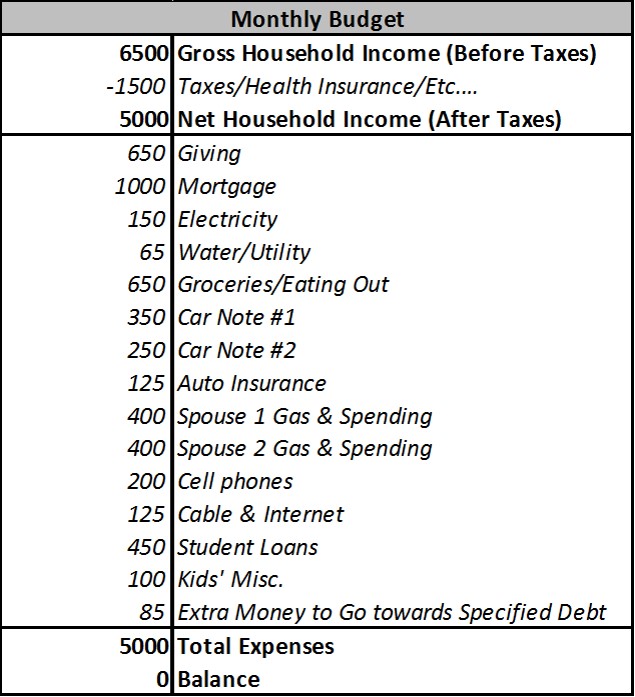

Below is an example of what a budget may look like.

Notice, the first line on this budget is “Giving”. I am a Christian and I believe in the principle of tithing first. So we give 10% off of our Gross Income, not our net. So in this example, the household gross income is $6,500, therefore, their tithe is $650, not $500. This is just what we do in our household, everyone is responsible for their own household. Also notice that we have a “Zero balance budget”. We do not have any money remaining on paper…every dollar is assigned a job. The extra money that was left over (in this example it was $85) can go to whichever debt you want to pay off first.

This is just an example of what a monthly budget may look like and I STRONGLY suggest you sit down (with your spouse, if applicable) and create a monthly budget for your own household.

In essence, PLAN AHEAD! Before you get your paycheck, already have a plan in place for how you will spend your paycheck. And if something unexpected comes up, adjust your plan accordingly. The point is to PLAN and stick to the PLAN each month.

To get more tips on organizing your finances, subscribe to our blog below and download our FREE CHEAT SHEET, “7 Steps to Building A Financial Legacy”.